Health savings accounts (HSAs) and flexible spending accounts (FSAs) are two types of savings accounts that help consumers pay for medical expenses. While these accounts have some qualities in common, these plans aren’t exactly alike. Here, we’ll break down the differences between healthcare HSA vs. FSA so you can determine which one is the best fit for your needs.

Healthcare HSA vs. FSA: Definitions

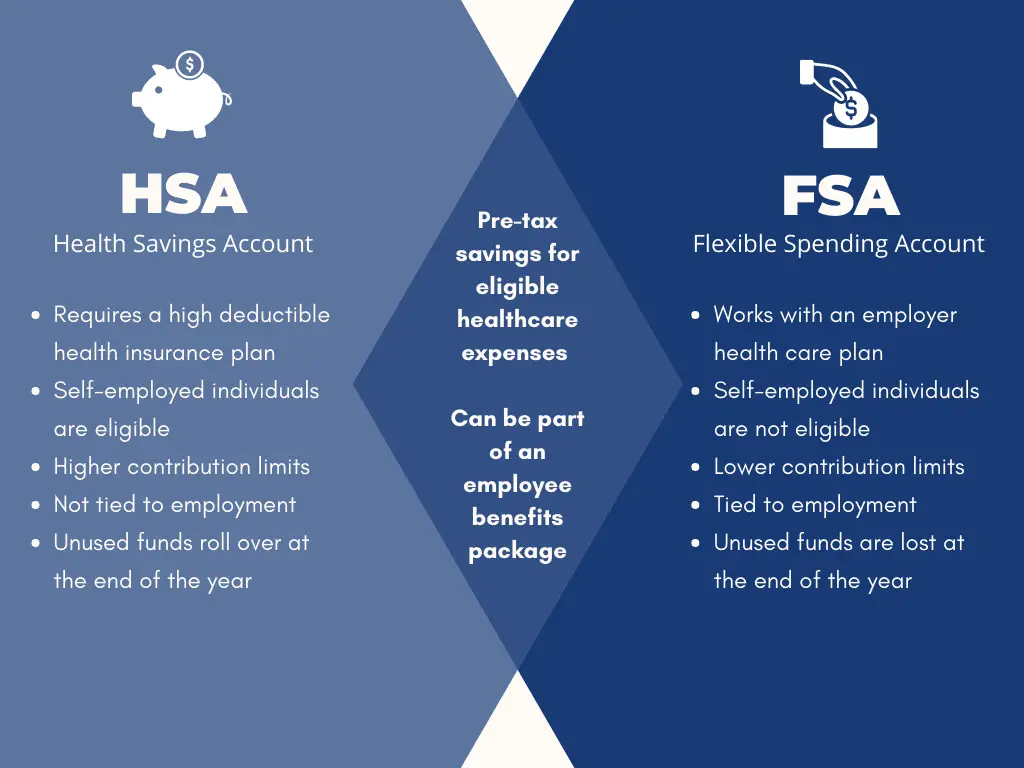

A Health Savings Account (HSA) is a savings account that enables you to set aside money to cover qualified medical expenses, tax-free. Eligible expenses include deductibles, copays, coinsurance, and other costs depending on your plan, allowing you to reduce the cost of health insurance. The account owner is the employee. If you are self-employed, you can contribute to HSA.

A Flexible Spending Account (FSA) is a health care savings account that also lets you set aside money for out-of-pocket expenses, just like the HSA does. Qualified expenses also include copays, coinsurance, and other costs depending on your plan. These accounts are typically part of an employer’s benefits package. If you are self-employed, you can not contribute to FSA.

How Does It Work?

Health Savings Accounts

An HSA works in combination with your employer’s health care plan, but you must have a qualified High Deductible Health Plan (HDHP) to be eligible. If you have an HDHP, for 2020, you can contribute the following amounts to an HSA:

- Up to $3,550 for self-only coverage

- Up to $7,100 for family coverage

For 2021, this amount will be $3,600 for self-only and up to $7,200 for family. If you are 55 or older, you can contribute $1,000 more annually.

Flexible Spending Accounts

A healthcare FSA works in combination with your employer’s health care plan. When you incur medical expenses that are not covered by your health care plan and have proof of the expense, you can submit a claim to your FSA through your employer for a health reimbursement arrangement.

When you enroll in an FSA, you decide your contribution amount deducted from your paycheck pre-tax for the year. This amount is binding for the plan year. However, if you have a qualifying life event (such as marriage or birth of a baby), you can enroll outside of the enrollment period into an FSA or adjust your contributions.

What Are the Benefits?

Health Savings Accounts

- HSA contributions are tax-deductible or pre-tax if paid via payroll deduction, giving you the capacity to pay for medical expenses with pre-tax money

- Interest can be earned on your HSA account and is non-taxable – provides an opportunity to build retirement savings that can be used for medical expenses

- If you withdraw for qualified medical expenses, you will not be taxed on that amount

- If you do not use all of the funds, they rollover, without limit, from year to year

- The HSA is owned by you and is yours to keep even if you change plans or retire

When you evaluate that your contributions are tax-deductible and if you withdraw for qualified medical expenses with no tax penalty, you can see how this saves you in the form of taxes.

Also, since you can earn interest on your fund, you can carry over what is not used from year to year, and you won the HSA even if you change plans or retire. It is an investment as well as preventative cost management.

When you reach age 65, there is no longer a deduction for withdrawing HSA funds to be used for non-medical purposes, but you will owe income tax on withdrawals.

Flexible Spending Accounts

- You can use the funds in your FSA for yourself, your spouse, or your dependents

- You can spend FSA funds on prescriptions and over-the-counter medicine prescribed by your doctor

- FSA funds may also be used for medical equipment like crutches, bandages, and diagnostic supplies like blood sugar test kits

- Your employer may make contributions to your FSA fund, but is not required to

- FSA contributions are not tax-deductible

What Are The Drawbacks?

Health Savings Accounts

One drawback of an HSA account is that you must have a High Deductible Health Plan (HDHP) to qualify. If you have significant health care expenses or expect to in the future, a high-deductible health plan may not be the best option for you.

Although you can contribute to an HSA fund, you may be better off with a health insurance plan with higher premiums but better coverage. Other drawbacks include:

- Budgeting accurately for unpredictable illness is difficult

- Finding out what the costs and quality of care beforehand is hard to find

- Setting aside money to put into your HSA fund can be challenging

- You may feel a need to save the money in your fund, and this may cause you to not seek needed medical care

- Money deducted for non-medical reasons is taxed

Note: One a person enrolls in Medicare, they are no longer allowed to contribute to an HSA. They can still withdraw tax-free funds from their HSA account to use for medical expenses, including Medicare premiums.

Flexible Spending Accounts

- The money in your FSA fund that is not used does not carryover at end of the year

- After the plan year, you lose any money left over in your account

- You can not spend FSA funds for insurance premiums

- If you lose your job, you lose your FSA account

- FSA accounts have a maximum contribution amount of $2,550 per year.

Special Grace Periods and Carry-Overs for FSA

Your employer may provide either a “grace period” of up to 2 1/2 months to use the money in your account, or let you carry over up to $500 to the following plan year. Your employer can provide only one of these options, and neither is required of your employer.

Which Plan is Right for You?

Now that you know the differences, benefits, and drawbacks concerning FSAs and HSAs, you need to decide which one is best for you. Remember that to qualify for an HSA, you must have a high deductible health plan. Once you are enrolled in an HDHP, the health insurance plan will likely refer you to a bank to house your HSA account.

However, you have the right to choose any bank account that you like. If you are not enrolled in a qualified HDHP, you will want to review the benefits and drawbacks of an FSA to decide if it works for your needs. Both types of healthcare accounts provide some tax benefits, and both can help pay for copays, prescriptions, coinsurance, and other expenses, depending on the plan.

Consider your current health status, your projected future health status, and the amount of take-home money you need to support yourself and your family, so when enrollment opens, you will be prepared.

Taking The Next Step

If you are interested in contributing to either of these healthcare savings accounts, you need to check with your employer about when open enrollment begins. Unless you have a qualifying life event, you will need to wait until open enrollment. In addition, ask your employer if they offer contributions to employee accounts.

That could be your deciding factor. Another question for your employer is about grace periods and carry-overs, as noted about FSAs. If your employer offers one of these options, it will figure prominently into your decision.